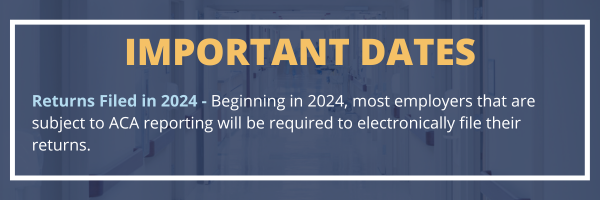

Based on the new ACA Reporting threshold, most employers must file electronically beginning in 2024.

The Affordable Care Act (ACA) created reporting requirements under Internal Revenue Code (Code) Sections 6055 and 6056. Under these rules, certain employers must provide information to the IRS about the health plan coverage they offer (or do not offer) to their employees.

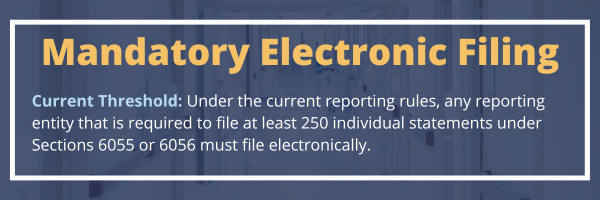

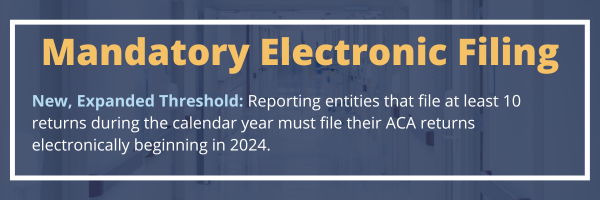

Currently, any reporting entity that is required to file at least 250 individual statements under Sections 6055 or 6056 must file electronically. However, on Feb. 23, 2023, the IRS released a final rule implementing a law change by the Taxpayer First Act of 2019, which lowers the 250-return threshold for mandatory electronic reporting to 10 returns. This means most reporting entities will be required to complete their ACA reporting electronically starting in 2024.

This ACA Compliance Bulletin describes the process for reporting electronically under Sections 6055 and 6056.

Action Steps

Employers that are subject to the ACA reporting rules should begin to explore options for filing ACA reporting returns electronically. For example, they may be able to work with a third-party vendor to complete the electronic filing.

Reporting entities that may be in a position to perform their own electronic reporting can review the IRS’ ACA Information Returns (AIR) Program main page for more information on the reporting standards for composing and successfully transmitting compliant submissions to the IRS.

ACA Electronic Reporting Requirement

For returns that must be filed in 2023, any reporting entity that is required to file at least 250 individual statements under Sections 6055 or 6056 must file electronically. The 250-or-more requirement applies separately to each type of individual statement. Entities filing fewer than 250 returns during the calendar year may choose to file on paper but are allowed (and encouraged) to file electronically.

Beginning in 2024, employers that file at least 10 returns during the calendar year must file their ACA returns electronically. Due to the lowered threshold, only the smallest employers will be permitted to file using paper returns. Reporting entities must aggregate most information returns, such as Forms W-2 and 1099, to determine if they meet the 10-return threshold for mandatory electronic filing.

Currently, electronic filing is done using the AIR Program. The IRS has provided a lot of guidance and information on electronic reporting under Section 6055 and Section 6056 through its AIR Program main page. However, this guidance is generally very technical and intended for software developers and other entities that plan on providing electronic reporting services. The IRS’ electronic filing guidance is not generally intended to be used by employers that are required to file under Section 6055 or Section 6056, but it can provide some useful information on standards and procedures for returns transmitted through the AIR Program.

AIR Program Overview

In general, the AIR Program is used by:

- Software developers who develop software for creating electronic files for ACA information returns;

- Transmitters who will transmit information returns to the IRS on behalf of reporting entities; and

- Issuers who have the capability to transmit information returns directly to the IRS on their own behalf.

In most cases, issuers, employers and other reporting entities will use a third-party vendor to file electronically with the IRS on their behalf. As a result, these entities will not directly use the AIR Program themselves.

ACA Electronic Reporting Process

The following steps must be completed by entities that submit electronic returns through the AIR Program:

- Step One: Register to use IRS e-Services tools (new sign-in options are now available) and apply for the ACA Application for Transmitter Control Code (TCC). The IRS issued a tutorial for requesting a TCC. Reporting entities that are using third-party vendors—and are not transmitting information returns directly to the IRS—should not apply for a TCC.

- Step Two: Pass all applicable test scenarios. Software developers are required to annually pass ACA Assurance Testing System (AATS) testing to transmit information returns to the IRS, and those who passed testing for any tax year ending after Dec. 31, 2014, do not need to test for the current tax year. Transmitters and issuers must use approved software to perform the communications test, which is only required to be successfully completed once.

Additional details and IRS resources are available on the IRS’ AIR Program main page.

Waiver From Electronic Filing Requirement

A hardship waiver may be requested from the electronic filing requirement by submitting Form 8508, Application for Waiver from Electronic Filing of Information Returns, to the IRS. Reporting entities are encouraged to submit Form 8508 at least 45 days before the due date of the returns, but no later than the due date of the returns. The IRS does not process waiver requests until Jan. 1 of the calendar year the returns are due.

Reporting entities cannot apply for a waiver for more than one tax year at a time and must reapply at the appropriate time for each year a waiver is required. Any approved waivers should be kept for the reporting entity’s records only. A copy of an approved waiver should not be sent to the service center where paper returns are filed.

If a waiver for original returns is approved, any corrections for the same types of returns will be covered under the waiver. However, if original returns are submitted electronically, but the reporting entity wants to submit corrections on paper, a waiver must be approved for the corrections if the reporting entity must file 250 or more corrections (for returns that must be filed in 2023 or earlier).

Without an approved waiver, a reporting entity that is required to file electronically but fails to do so may be subject to a penalty of up to $290 per return (as adjusted annually) unless it can establish reasonable cause. However, reporting entities can file up to 250 returns on paper (for returns that must be filed in 2023 or earlier); those returns will not be subject to a penalty for failure to file electronically. The penalty applies separately to original returns and corrected returns.

For further questions, contact RMC Group today at 239-298-8210 or rmc@rmcgp.com.

This article is not intended to be exhaustive, nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice. ©2023 Zywave, Inc. All rights reserved.

-Jun-01-2026-09-11-11-7643-PM.png)

-May-28-2026-04-06-00-2941-PM.png)