Now is the time to act if they want to defer for 2022!

Business owners are always on the lookout for ways to save money. They’re also interested in retirement plans as a way to have a financially secure retirement when they no longer want to work. And if they have employees, they’re also interested in providing a way for them to save for retirement as well.

A good vehicle for retirement savings? A 401(k) plan. 401(k)s are the most popular retirement plans in the U.S. today. According to the Investment Company Institute, as of September 30, 2021, 401(k) plans held $7.3 trillion in assets for over 60 million active participants and millions of retirees and former employees in about 600,000 plans.

Why are 401(k) plans so popular? Why should a small business owner look at sponsoring one as part of their benefits package? Offering a 401(k) plan provides generous perks for employers and tax-deferred benefits for their employees. A 401(k) plan allows a business owner to save on personal taxes through tax-deferred contributions and if they qualify, they can take advantage of the business tax credits from the Setting Every Community Up for Retirement Enhancement Act (SECURE Act) to cover the cost.

Background

401(k) plans are intended to benefit all employees, not just the owner or other highly paid employees. As a result, the Internal Revenue Code requires that employers perform annual Actual Deferral Percentage (ADP) and Actual Contribution Percentage (ACP) non-discrimination tests. If a plan fails either of these tests, the amount that highly compensated employees can defer is reduced or additional contributions must be made for the benefit of rank-and-file employees to keep the plan in good standing. In addition, if more than 60% of the assets belong to 5% owners and/or certain officers, minimum contributions are required to be made for the other employees, or highly compensated employees will be unable to make deferrals to the plan.

Safe Harbor 401(k)s

In order to avoid discrimination testing, an employer can adopt a Safe Harbor 401(k) plan. Safe Harbor 401(k)s are a lot like traditional 401(k) plans, but with some key differences. A Safe Harbor 401(k) plan requires guaranteed minimum company contributions. This allows the plan to sidestep non-discrimination testing.

Any size company can adopt a Safe Harbor 401(k) Plan, but they’re especially popular with small businesses (under 100 employees) that would otherwise have difficulty passing non-discrimination tests.

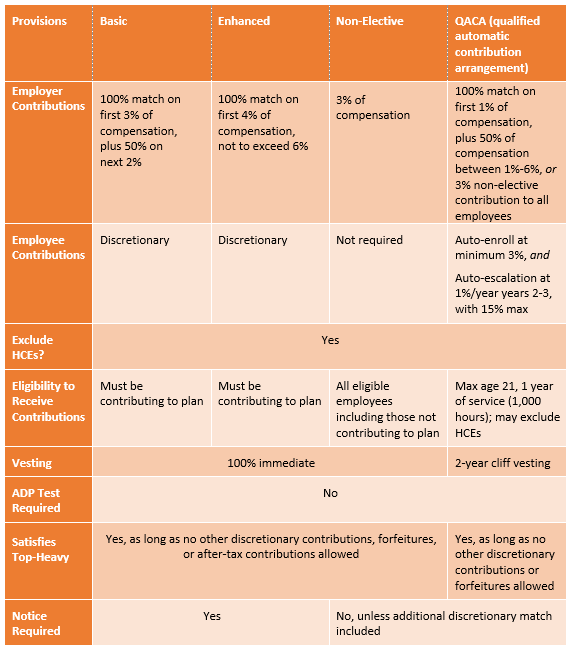

There are four types of Safe Harbor matching formulas. Business owners can choose which formula they want, providing them flexibility in having the plan design that best fits their needs and their budgets.

Safe Habor 401(k) Plan Formulas

Advantages of Safe Harbor 401(k)s

Safe Harbor 401(k) plans have lots of advantages, both to their plan sponsor/business owners and their employee participants including:

- No Non-Discrimination Testing – The biggest advantage of a Safe Harbor plan is no annual non-discrimination testing. In exchange for fixed employer contributions and participant disclosures, the plan is either exempt from expensive and time-consuming ADP/ACP non-discrimination tests (plus satisfies top-heavy minimum contribution requirements) or automatically passes them.

- Higher Contributions – Thanks to no non-discrimination testing all employees can contribute the maximum amount into their account ($20,500 in 2022 with an additional $6,500 in catch-up contributions for those age 50+) without having to worry about having their contributions capped at a lower amount or, worse, being returned as corrective distributions if the plan does not pass the ADP/ACP non-discrimination tests.

- Flexible Matching Formulas – With the Non-Elective formula, every employee receives 3% of their compensation into their plan account. And if they contribute toward their own retirement, they can receive up to an additional 4% of their compensation in matching contributions.

- Employee Recruiting and Retention – A Safe Harbor 401(k) plan is a powerful incentive to attract and keep key employees.

- Tax Benefits – Safe Harbor plans provide the same tax benefits to business owners and employees as a traditional 401(k) plan does. In addition, owner contributions are tax-deductible up to 25% of compensation per employee. In 2022, compensation is limited to $305,000.

- Saving Incentives – The required company match encourages employees to save for their own retirement.

- Profit-Sharing Enhancement – Owners can add a profit-sharing feature to their Safe Harbor Plan to further increase contribution levels, though this may require a vesting schedule.

Disadvantages to Safe Harbor 401(k)s

On the flip side, Safe Harbor 401(k) plans do have some disadvantages to the benefits above:

- Higher Costs – A Safe Harbor plan requires regular employer contributions, either on a per-payroll basis or at the end of each plan year. Businesses need to have steady stream of income to meet these contributions or the plan will lose its tax-qualified status. It’s possible that required contributions could increase payroll costs by 3% or more if all the employees participate.

- Administrative Complexity – Safe Harbor plans are more complex to administer despite not having to run non-discrimination tests. For example, they require annual notices to all participants at least 30 days before the end of every plan year which can add an administrative burden to the owner.

Setting up a Safe Harbor 401(k)

As with any qualified plan, your clients should know all their options so they can make the best choice in plan designs for them and their business. You’re their guide as they go through the decision and setup process.

The process for establishing a Safe Harbor 401(k) plan is the same as the process for establishing a traditional 401(k) plan. October 1 is the deadline for a 2022 Safe Harbor 401(k) plan to be operational. Setting up a new plan takes time, so it’s best not to wait until the last minute.

- Determine if a Safe Harbor 401(k) plan is best for your clients’ needs. Several factors can help in this process:

-

- Total number of employees in the company and their anticipated deferral rates

- Cost estimates under each of the four Safe Harbor formulas

- Number of highly compensated employees who may want to contribute maximum amounts

-

- Decide on plan provisions and develop a written plan document at least 45 days before the plan’s start date

- Send notices to all employees of their rights and obligations under the plan at least 30 days before the plan’s start date

- Determine investment lineup

- Enroll employees

- Plan is operational by October 1

A Safe Harbor 401(k) plan offers real advantages over a traditional 401(k). Business owners need to assess their needs and how a Safe Harbor 401(k) can help them and their highly compensated employees’ squirrel away more retirement money than they could under a traditional 401(k).

Conclusion

In the end, though, many employers think the benefits of offering a Safe Harbor 401(k) plan more than outweigh the cost. There’s peace of mind at not having to worry about their plan failing its non-discrimination tests. Sponsoring a Safe Harbor 401(k) plan shows the owner cares about their employees’ retirement security resulting in more appreciative employees.

401(k) plans give business owners many ways to save and design their plan. Selecting a Safe Harbor design is very personal, taking into consideration the cost versus ultimate benefit to the owners and their employees. Wise business owners will work with an advisor to craft a plan that will help them meet their retirement savings goals, as well as the goals of their employees.

We in the Pension Division at RMC Group specialize in working with advisors who serve the small plan market. We can help you market, set up, and administer your clients’ Safe Harbor 401(k) plan.

Call 239-298-8210 or visit our website at rmcgp.com to discover how we can partner with you to help small business owners successfully set up and administer a Safe Harbor 401(k) plan that will maximize their savings and tax deductions.

The clock is ticking if you want to start a 401(k) Plan with a Safe Harbor design for a client. The deadline for having the plan operational is October 1, 2022, because employees must be given at least three months to make deferral contributions.

However, the deadline to start the process is just ahead – August 15th. That’s to allow time to draft the plan document and paperwork and to give employees the required 30-day notice that a plan is being installed.

-Jun-01-2026-09-11-11-7643-PM.png)

-May-28-2026-04-06-00-2941-PM.png)