The Complexities and Opportunities in Long-Term Part-Time Employee Regulations

In a significant development, the Department of the Treasury and the Internal Revenue Service published proposed regulations setting forth rules for the treatment of long-term part-time employees (LTPTE) in qualified retirement plans. Released on November 24, 2023, with an effective date of January 1, 2024, the regulations provide crucial guidance on eligibility, vesting, and administration for 401(k) plans.

The SECURE 2.0 Act: A Brief Overview

To understand the context, we trace back to the SECURE 2.0 Act, enacted on December 29, 2022. Building upon its predecessor, SECURE Act of 2019 which was passed into legislation in 2019, amended previous requirements and aimed to bolster retirement planning for long-term, part-time employees. The focus is on ensuring financial wellness and closing the retirement gap among this segment of the .

Long-Term Part-Time Employee Eligibility

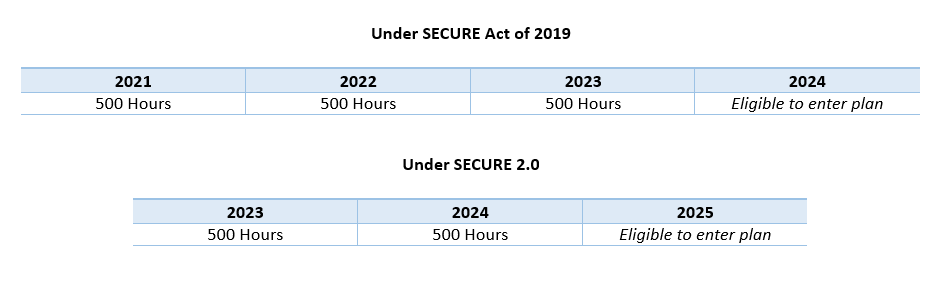

Under SECURE 2.0, a long-term part-time employee is defined as an individual who completes 500 hours of service for two consecutive years. Notably, each 12-month period of service for which the employee has at least 500 hours will be counted for eligibility and vesting in employer This marks a departure from the previous three-year requirement under SECURE Act of 2019.

The Transition Period

For those familiar with the SECURE Act of 2019, the transition from the older rule to the new two-year requirement brings practical implications. Employees qualifying under the previous rule will be eligible for elective deferrals in 2024, while those meeting the new two-year requirement will have to wait until 2025.

Special Rules for LTPTEs

The proposed regulations introduce special rules for LTPTEs, impacting coverage tests, nondiscrimination tests, top-heavy contributions, and vesting computations. Some key points include:

- LTPTEs can be disregarded for the 410(b) coverage test.

- They may be disregarded for ADP and ACP tests, including eligibility for ADP test safe harbor contributions.

- No minimum top-heavy contributions are required, but they are included in calculating the top-heavy ratio.

- LTPTEs earn vesting service for each year with at least 500 hours of service, even without employer contributions.

- Vesting for Current and Former LTPTEs.

The proposed regulations provide clarity on vesting service for LTPTEs, emphasizing the strict interpretation that all LTPTEs will earn vesting service using the 500-hour rule. This applies even if they do not receive employer contributions as LTPTEs. The complexity arises when an LTPTE becomes a full-time employee, as the 500-hour rule continues to apply.

Impact on Safe Harbor Plans

For safe harbor plans with service-based eligibility conditions, the new regulations present administrative and design challenges. Plans with more liberal service conditions or without service conditions aligned with LTPTE rules may continue without significant changes.

Effective Date and Plan Corrections

The proposed regulations are set to apply to plan years beginning on or after January 1, 2024. Taxpayers can rely on the regulations until further guidance is issued. However, it’s crucial for plans to navigate potential inadvertent violations promptly. Plan corrections will be essential to address any oversights in permitting affected employees to make salary deferrals.

Conclusion

As the retirement planning landscape undergoes substantial changes with the introduction of SECURE 2.0 and its proposed regulations, plan sponsors and administrators must stay informed and take necessary actions. The changes made by the SECURE 2.0 Act brings both opportunities and challenges, and a thorough understanding of the rules is essential for compliance. For more updates on SECURE 2.0, join our monthly newsletter here.