As we previously reported, on December 29, 2022, President Biden signed the Consolidated Appropriations Act, 2023, which funds the government for the fiscal year that began on October 1, 2022. Embedded in that legislation, as Division T, was the SECURE 2.0 ACT of 2022 (the SECURE Act 2.0). The final version of the SECURE Act 2.0 reconciled separate bills passed by the House and the Senate during 2022.

The SECURE Act 2.0 includes over ninety provisions designed to enhance the retirement savings of American workers. Some of its provisions take effect immediately. However, others do not become effective until plan years commencing after December 31, 2023, or even later. In addition, some of the provisions are mandatory, and some are permissive. One of the provisions that does not become effective immediately is Section 103 of the SECURE Act 2.0, which makes changes to the so-called Saver’s Credit to provide greater incentives for workers to save for retirement.

The Problem

Congress has long recognized that many Americans do not have sufficient retirement savings. In addition, Congress has recognized that the problem is twofold. On the one hand, many employers are either unable or unwilling to adopt a qualified retirement plan because they think the start-up and on-going administration costs will be prohibitively expensive. On the other hand, even when employers do offer qualified retirement plans, many employees decline to participate because they think that they cannot afford to make contributions.

As we discussed in a previous article, Congress addressed the employer side of the equation in Section 102 of the SECURE Act 2.0 by enhancing the credits for costs incurred by an employer in connection with the establishment and ongoing administration of a qualified retirement plan.

This article will discuss Section 103 of the SECURE Act 2.0, where Congress addressed the reluctance of employees to save for retirement when that requires the deferral of current income.

What is the Saver’s Credit?

Under current law, individuals are eligible for a tax credit for contributions to an Individual Retirement Account (IRA) or their employer’s qualified retirement plan. This is known as the Saver’s Credit and is found in section 25B(a) of the Internal Revenue Code:

In the case of an eligible individual, there shall be allowed as a credit against the tax imposed by this subtitle for the taxable year an amount equal to the applicable percentage of so much of the qualified retirement savings contributions of the eligible individual for the taxable year as do not exceed $2,000.

While section 25B(a) seems straightforward, it does raise a number of questions. The first issue is “who is an eligible individual?” An eligible individual is a person who:

1. is over 18 years of age;

2. is not claimed as a dependent by another taxpayer; and

3. is not a student.

A student is a person who:

1. is a full-time student at a school; or

2. is enrolled on a full-time basis in an on-farm training program.

The term school includes a technical, trade and mechanical school but does not include on-the-job training.

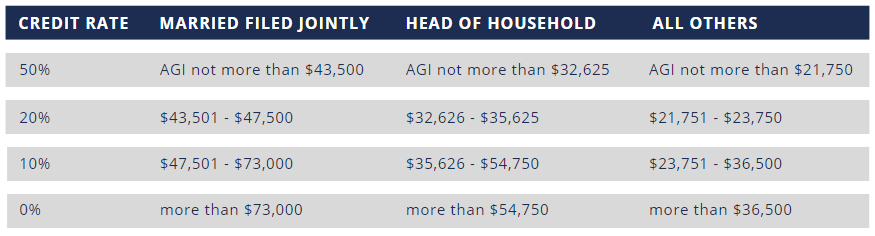

The next question is “how much is the credit?” That depends on the taxpayer’s adjusted gross income (AGI) and filing status. The amount of the credit is a sliding scale that decreases as the taxpayer’s income increases. For 2023, the amount of the credit is as follows:

To illustrate the foregoing, assume that an individual had an AGI of $40,000. Also assume that she is married and filing jointly but her husband had no income for the year. Finally, assume that she made a salary deferral of $4,000 to her employer’s 401(k) plan. (Because she is married and filing jointly, the maximum contribution that can qualify for the credit is $4,000, not $2,000.)

Since her adjusted gross income is not more than $43,500, her credit is 50% of her contribution or $2,000. If her adjusted gross income had been $45,000, her credit would be 20% of her contribution or $800, and if her adjusted gross income had been $60,000, her credit would be 10% of her contribution or $400. Finally, if her adjusted gross income had been $75,000, she would be entitled to no credit.

What is a Tax Credit?

The Saver’s Credit is, without doubt, a valuable benefit to those individuals who qualify for it. However, not every taxpayer is eligible for the Saver’s Credit. As we have seen, there are income limitations, and the Saver’s Credit is phased out at higher incomes. But that is not the only problem with the Saver’s Credit.

A tax credit is a dollar-for-dollar reduction of the taxes owed by a taxpayer. Assume a tax credit of $100 and taxes due of $1,000. The tax credit reduces the taxpayer’s tax obligation to $900. In that sense, it puts money in the taxpayer’s pocket. However, what if a taxpayer does not owe any taxes? And, in fact, many lower-income taxpayers owe no taxes at the end of the year. What happens to their tax credit? It disappears. The Saver’s Credit is a non-refundable tax credit. So, unless a taxpayer has tax due against which to offset the Saver’s Credit, the taxpayer gets no benefit from the Saver’s Credit. It is not paid in cash to a taxpayer who owes no taxes.

What is the Saver’s Match?

Section 103 of the SECURE Act 2.0 eliminates the Saver’s Credit and substitutes a government match. Instead of a credit against taxes owed by the taxpayer, the Saver’s Match is a payment to the taxpayer’s retirement account. Section 103 of the SECURE Act 2.0 added section 6433 to the Code, which provides in subsection (a)(1) that:

Any eligible individual who makes qualified retirement savings contributions for the taxable year shall be allowed a matching contribution for such taxable in an amount equal to the applicable percentage of so much of the qualified retirement savings contributions made by such eligible individual for the taxable year as does not exceed $2,000.

This provision converts the Saver’s Credit into a Saver’s Match. It means that the federal government will deposit the amount of the Saver’s Match into a taxpayer’s retirement account, whether an IRA or an employer’s qualified retirement plan, whether or not the taxpayer owes any taxes. The Saver’s Match is subject to many of the same requirements and restrictions as the Saver’s Credit. However, there is one huge difference. Every eligible taxpayer will receive the Saver’s Match, not just those who owe taxes at the end of the year.

The changes made by Section 103 of the SECURE Act 2.0 are effective for plan years beginning after December 31, 2026.

Conclusion

There is no question that a qualified retirement plan is a valuable employee benefit. It helps an employer attract and retain workers. In addition, it helps employees to save for their retirement. However, many employers have shied away from adopting a qualified retirement plan because of the cost.

In addition, many employees do not participate because they are unwilling to defer current income for retirement income. In the SECURE Act 2.0, Congress addressed both issues. Section 102 provides enhanced tax credits for employers to offset the start-up and administration costs of adopting a qualified retirement plan. Section 103 provides a federally-funded, matching contribution to those employees who make contributions to their retirement accounts. This is like “found money”. There is no longer any excuse for an employer to not adopt a qualified retirement plan or for an employee to not contribute to a retirement account.

For more information and to speak with a Retirement Professional, contact RMC Group at 239-298-8210 today!