The big push for defined contribution plans, such as 401(k)s, is designed to encourage employees to save as much as possible while they are working so they have a nest egg for their retirement years. Auto-enrollment and auto-escalation are tools employers use to ensure that employees participate in their retirement plans.

Auto-enrollment and auto-escalation may take care of the accumulation phase, but what about decumulation? That’s where obstacles may arise.

Decumulation Issues

The term “decumulation” means disposing of what has been accumulated. In the context of retirement plans, it refers to the process of distributing the plan’s assets after an employee retires.

The ways in which an employee can take distributions from a retirement plan are set forth in the plan document. Most plans limit the available distribution options in order to ease administration and costs. However, most plans offer a lump-sum option. In fact, this is typically the most common option, as most employees will transfer their 401(k) account to an IRA upon retirement. When this happens, the employee becomes responsible for managing their account and making sure that it lasts for the remainder of their lives.

But how good is the average employee as a money manager, and how equipped are they to manage their funds over many years? How are they to know how long they need their money to last or how long it will last at a certain withdrawal rate?

Retiring participants need help with the decumulation phase. However, until recently, plan sponsors had no obligation to help their employees, and most plan sponsors didn’t offer any help. Participants in 401(k) plans have needed, but haven’t had a way to estimate how much retirement income their plan account would provide. Until now!

SECURE ACT to the Rescue

Enter the Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE Act).

The SECURE Act included three provisions to encourage the adoption of guaranteed income products:

- Lifetime income disclosures to plan participants

- Fiduciary safe harbor for the prudent selection of lifetime income providers

- Portability of lifetime income

The first change the SECURE Act made sets the stage. This provision requires plan sponsors of ERISA-covered defined contribution plans, such as 401((k), 403(b), and profit-sharing plans, to include a lifetime income disclosure in participant statements at least once a year. The purpose of the lifetime income disclosure is to provide an estimate of the monthly income that the participant’s current account will provide after retirement.

The lifetime income disclosure was required to be included in participant statements for the first time for the second quarter of 2022 or June 30, 2022. So, the first statements containing lifetime income disclosures should now be in participants’ hands.

What do these lifetime income disclosures look like and how might participants react to them? Let’s find out.

Lifetime Income Disclosures

The lifetime income disclosure requirements provide a set of assumptions to be used in preparing the disclosures, as well as model language to use in the explanation.

First, the disclosure is to be written in a “manner calculated to be understood by the average plan participant” and must include:

- The statement period beginning and ending dates

- The participant’s account balance as of the last day of the statement period, expressed as a lifetime income stream payable in equal monthly payments as both a single life annuity (SLA) and qualified joint and survivor annuity (QJSA)

Disclosure Assumptions

The DOL has prescribed certain assumptions that must be used in the disclosures. These assumptions include:

- Annuity start date – the last day of the benefit statement period

- Age on annuity start date – age 67 or actual age if greater than 67

- Single life annuity

- Fixed monthly income for the life of the participant

- No survivor benefit paid after the participant’s death

- Qualified joint and survivor annuity

- Fixed monthly amount for the life of the participant and 100% of the amount to the surviving spouse after the participant’s death

- Participant has a spouse of the same age (regardless of actual marital status or actual age of any spouse)

- Interest rate – the 10-year constant maturity Treasury rate (10-year CMT) as of the first business day of the last month of the statement period

- Mortality – Unisex mortality as described in Internal Revenue Code (IRC) Section 417(e) for defined benefit plans

- Participant loans – account balance includes outstanding loans not in default

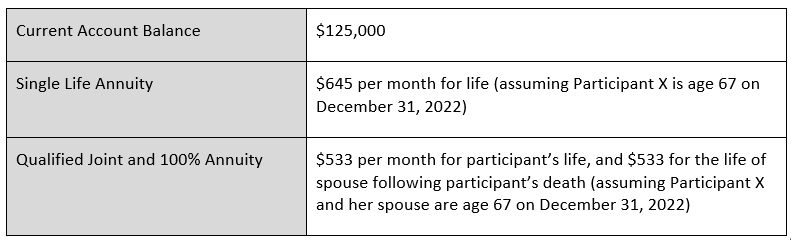

Example

The Department of Labor (DOL) Employee Benefits Security Administration (EBSA) has provided an example which illustrates the application of the regulatory assumptions (Table 1).

Participant information: Participant X is age 40 and single. Her account balance on December 31, 2022, is $125,000. The 10-year CMT is 1.83% per annum on the first business day of December. The benefit statement of this participant would show the following:

Table 1. Lifetime Income Disclosure Assumptions Example

Lifetime Income Disclosure Participant Issues

So, now that the first lifetime income disclosures have been sent, have participants even noticed? And if so, what did they think about them? Have any problems been identified?

The first reaction may have been shock – to discover how little their account balances would provide in retirement income – a lot less than they had initially thought, since, as discussed above, the disclosures assume the every participant is age 67 and don’t take into account future contributions or investment gains.

Employees are going to need help understanding the disclosures. Here’s where you as an advisor can shine. You know how the disclosures work and can help participants understand them and their purpose.

Clarify the Disclosures

In addition, you understand annuities and can explain how they can be used to provide a stream of income after retirement. You can also clarify the disclosures:

- Participants need to understand what’s included in their projections and what’s not. Factors such as interest rates, contributions, and fluctuations in investment returns can cause the illustrations to change from one statement to the next.

- Older participants, closer to retirement, might be confused when the projected income on their statements is higher than their actual income will be. That’s because the projections assume that the entire balance has been annuitized.

- Employees who have changed jobs frequently and have rolled their retirement account to an IRA after every job change won’t have anything close to an accurate representation of what their lifetime income stream could be. That’s because their lifetime income projections only represent their current plan and account balance. There’s no way to include IRA balances.

Participant responses can vary from those who don’t even look at their statements to those who only read the first page and don’t see the explanations on subsequent pages to those who understand the illustrations and what they mean.

Takeaways

These new disclosures are good news for advisors. Plan sponsors and plan participants are going to need help understanding them. That is something that you as an advisor are particularly qualified to do.

By helping employees understand how to make their retirement account last through their retirement years by using lifetime income products, you’re also helping yourself. You’ll grow your business with new clients and have a good feeling about having helped them have a better retirement.

Follow along for part 2 of this article to read about fiduciary safe harbor for the prudent selection of lifetime income providers and the portability of lifetime income benefits.

Solution

The Pension Division at RMC Group specializes in working with advisors who serve the small plan market and its participants. We can help you market and set up presentations and programs that explain to an employee what their lifetime income disclosures are all about, as well as best practices in selecting a lifetime income provider and helping participants handle their product’s portability issues.

Call 239-298-8210 or visit our website at rmcgp.com to discover how we can partner with you to help employees successfully understand their retirement statements.

-Jun-01-2026-09-11-11-7643-PM.png)

-May-28-2026-04-06-00-2941-PM.png)