Small business owners often don’t have a retirement plan – for their employees or, more importantly, for themselves. Often, they are too busy running their business, putting any money they have back into the business, or they think a retirement plan is too expensive and too complex.

As a result, they often end up with no retirement planning strategy or one that does not come close to meeting their needs. But they don’t have to.

If you haven’t read part one yet, read that here first.

Two Plan Options

Business owners have a variety of qualified retirement plans to choose from. But what is a qualified retirement plan?

A qualified retirement plan is an employer-sponsored plan that meets the design requirements of the Internal Revenue Code and as a result, provides certain tax advantages to both the employer and its employees. Contributions made by the employer may be tax deductible and not includible in an employee’s income until paid out after retirement.

Depending on the type of plan adopted by the employer, employees may contribute to the plan as well. Plus, employee contributions can be on a before-tax basis with tax-deferred earnings. If a plan permits Roth deferrals, contributions are made on an after-tax basis, but distributions can be tax-free.

There are two broad categories of qualified retirement plans:

- Defined Contribution Plan – a plan in which the contributions are defined up front and the final benefit is a participant’s accumulated account balance

- Defined Benefit Plan – a plan which provides a guaranteed monthly benefit for life that’s based on a formula that is some combination of an employee’s age, compensation, and/or service

In addition, an employer can combine two types of plans in order to provide larger contributions and greater retirement benefits. The different types of qualified retirement plans include:

- 401(k)/Profit-Sharing Plan (Defined Contribution Plan)

- Traditional Defined Benefit (Defined Benefit Plan)

- Cash Balance Plan (Defined Benefit Plan)

- 412(e)(3) Defined Benefit Plan (Defined Benefit Plan)

Let’s Start With a 401(k) Plan

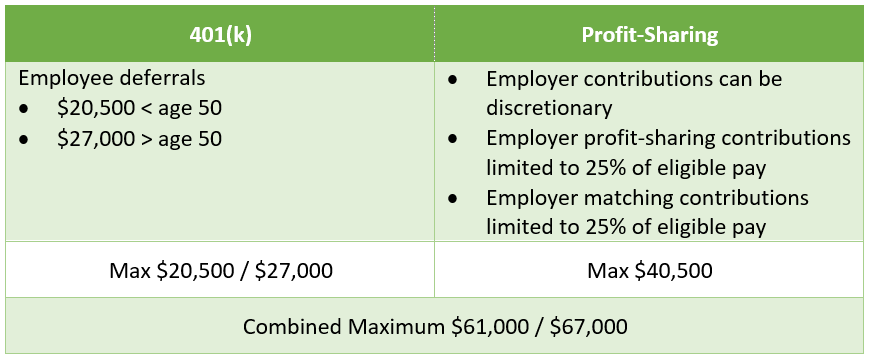

401(k) plans are the most common defined contribution plan around today. A 401(k) plan can allow for both employee deferrals and employer contributions. Total contributions to a 401(k) plan are limited to $61,000 in 2022, plus a catch-up contribution of $6,500 for employees age 50+ (or 100% of compensation, whichever is less). This limit applies to the total of:

- Employee salary deferrals – up to 100% of compensation to a maximum of $20,500 in 2022, $27,000 if age 50+

- Employer matching contributions – up to a maximum of 25% of eligible pay or the annual contribution limit, whichever is less (matching amounts are calculated based on employee salary deferrals)

- Employer non-elective contributions – up to a maximum of 25% of eligible pay or the annual contribution limit, whichever is less (non-elective contributions are calculated based on the employee’s eligible pay and not conditioned on deferrals to the plan)

A small business owner or solopreneur with no employees, other than perhaps a spouse, can establish a Solo 401(k) plan with the same limits.

Table 1. 401(k)/Profit-Sharing Plan Combo

2022 Limits

Retirement Strategies – Thinking Outside the Box

But even a 401(k) plan might not provide an owner with sufficient retirement funds.

Fortunately for small business owners, 401(k) plans aren’t the only kid on the block. Business owners who are looking for ways to save more for their retirement and make up for lost time have other options.

Traditional Defined Benefit or Cash Balance Plan

A defined benefit plan generally provides a greater retirement benefit than a defined contribution plan. However, benefits are still limited by the Internal Revenue Code. The maximum annual retirement benefit that a defined benefit plan may provide is limited to the lesser of:

- $245,000 (2022), or

- 100% of the participant’s average compensation for the highest three consecutive calendar years

A defined benefit plan requires annual contributions that are based on actuarial calculations.

For many years, defined benefit plans have fallen out of favor. However, they have recently been revived by the popular cash balance plan. A cash balance plan is a hybrid plan that looks like a defined contribution plan where benefits are expressed as a “hypothetical account balance” which is equal to earned “pay credits” and “interest credits” but acts as a defined benefit plan because it provides a guaranteed benefit at retirement.

- A cash balance plan allows for substantially higher tax-deductible contributions than a 401(k)/profit-sharing plan depending on age and works best for an owner aged 50 to 65. Benefits in a cash balance plan are subject to the same limits as a traditional defined benefit plan

Under normal circumstances, a business owner should be prepared to maintain a cash balance plan for at least five years to establish its permanency.

Cash balance plans are valuable savings vehicles for high-earning, small business owners who have put off saving for retirement, and who need to accumulate savings in as short a period as possible.

Cash Balance/401(k)/Profit-Sharing Plan

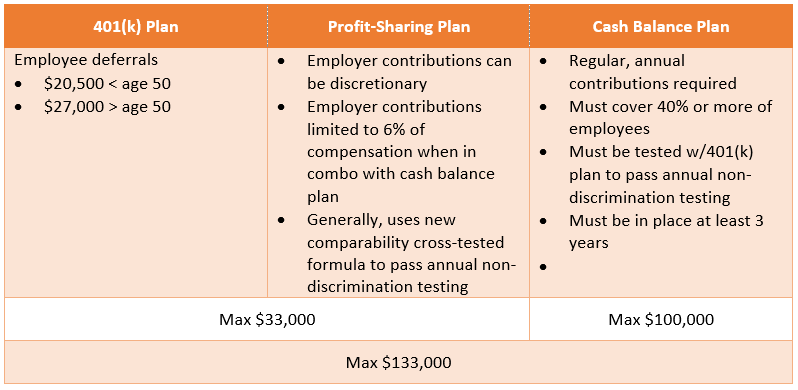

Another very favorable option for the small business owner is a cash balance plan combined with a 401(k)/profit-sharing plan.

This combination presents the best of both the defined contribution and defined benefit worlds. By maxing contributions to both plans, an owner can greatly increase his total annual retirement contributions, with the possibility of creating a substantial lifetime balance even with a W-2 salary of $100,000 (Table 2).

Table 2. 401(k)/Profit-Sharing/Cash Balance Plan Combo

Owner-Employee Age 50 with W-2 Wages of $100,000*

2022 limits

Important: when paired with a cash balance plan the profit-sharing contribution is limited to 6% of compensation instead of the usual 25% unless the plan is covered by the Pension Benefit Guaranty Corporation (PBGC). This chart assumes a plan that is not covered by the PBGC.

412(e)(3) Defined Benefit Plan

A 412(e)(3) plan is a type of defined benefit plan. Like other types of defined benefit plans, the plan’s benefits are determined according to a formula set forth in the plan document and based on employees’ compensation, age, and service. In addition, the plan’s benefits are funded by the employer. No employee contributions are allowed.

What’s different is that a 412(e)(3) plan is funded exclusively with annuity contracts or a combination of whole life insurance and annuity contracts that have guaranteed rates of return. Because these investment vehicles are fully insured, the plan doesn’t need an actuarial review, nor is it subject to minimum funding requirementIn addition, the amount of life insurance must be “incidental.”

Contributions to a 412(e)(3) plan are generally much higher than contributions to a traditional defined benefit plan or a defined contribution plan. A 412(e)(3) plan is ideal for small business owners who want to save as much as possible on a tax-deferred basis. A 412(e)(3) plan also allows an employer to make larger contributions for older employees, such as the owner, without increasing costs for younger employees.

A 412(e)(3) plan can also be used in conjunction with a 401(k) plan, allowing the owner an additional vehicle to max out contributions, so the owner can accumulate substantial retirement savings.

Conclusion

As we’ve seen, one size doesn’t fit all small business owners. Which savings plan a business owner selects is very personal, taking into consideration the cost versus ultimate benefit for himself and his employees. A wise owner will work with an advisor to craft a plan that will help him meet his and his employees’ retirement savings goals.

We in our Pension Division at RMC Group specialize in working with advisors who serve the small plan market. We can help you market, set up, and administer your clients’ qualified retirement plan.

Call 239-298-8210 or visit our website at rmcgp.com to discover how we can partner with you to help small businesses successfully set up and administer a qualified plan that will maximize their retirement savings.

-Jun-01-2026-09-11-11-7643-PM.png)

-May-28-2026-04-06-00-2941-PM.png)