The cost of college has gradually gone up over the past 30 years. And as college tuition has risen, so too has student loan debt. Student debt is so high that some call it a crisis.

Student Loan Debt: A Crisis

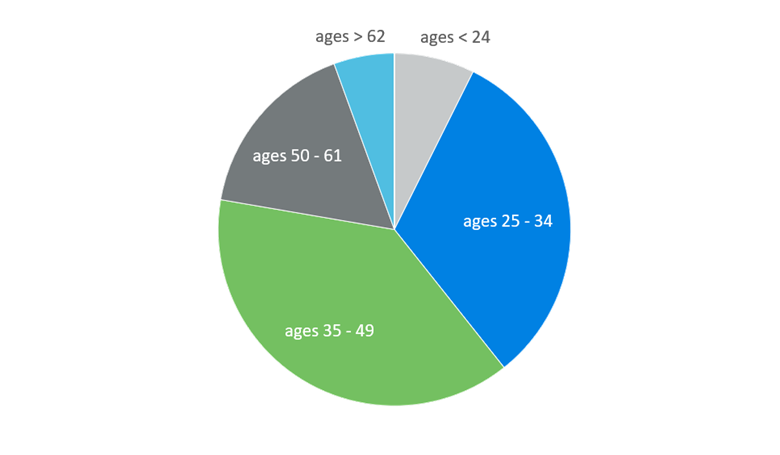

The student loan crisis affects about 45 million Americans who owe a massive $1.75 trillion in student loan debt as of 2021 according to the Federal Reserve. Surprisingly, it’s not the Millennials with the most student debt – it’s the age 35-49 cohort who owe $622 billion in federal loans (Chart 1).

Baby Boomers carry a lot of debt as well. In 2021, nearly nine million workers age 50+ still had student debt, either from loans they took out for themselves or loans they took for their children’s education, according to data from the Department of Education.

Chart 1 – Percent of Total Student Debt by Age Group

Source: December 2020 CNBC report

And how are students who graduated in 2021 going to repay loans that average $37,693, an amount that can take up to 20 years to pay, and still save for retirement?

Stay tuned.

How the 401(k) Match to Pay Off Student Loans Originated

Section 111 of the Secure Act 2.0, which passed the House on March 29, 2022, addresses student loan debt by treating “qualified student loan payments” as 401(k) employee deferrals, meaning that an employer can make matching contributions when an employee makes qualified student loan payments.

Secure 2.0 will help employees accumulate savings through their employer’s 401(k) match while they make student loan repayments, it’s not a new idea.

The root of Section 111 is a 2018 IRS Private Letter Ruling (PLR), 201833012, issued to health care company Abbott Laboratories on May 22 (made public on August 17). Abbott requested the ruling because they wanted to make 401(k) matching contributions to its employees who were paying off student loans.

401(k) plan matching contributions are generally based on the amount plan participants defer to their accounts. But participants saddled with the burden of student loan debt have a hard time contributing to their employer’s 401(k) plan, thus also missing out on matching contributions. It makes it hard for them to accumulate enough savings for a financially secure retirement

Abbott’s plan provided a 5% match into the company’s 401(k) plan for any employee who made payments of at least 2% of their pay toward their student loan debt via payroll deduction. This was the same match percentage Abbott gave to participants who contributed at least 2% of their pay to their 401(k) – the minimum contribution required to participate in the plan.

There was a major concern, however – how to make matching contributions when there weren’t any employee deferrals without violating the IRS’ “contingent benefit rule”:

- Under the contingent benefit rule, benefits, inside or outside of the plan, may not be contingent on an employee’s election to defer or not to defer

- Matching contributions are the only exception

In the PLR, the IRS determined that Abbott’s program didn’t violate that rule.

The PLR, though only applicable to Abbott and its 401(k) plan, caused quite a stir.

One of these was the Retirement Parity for Student Loans Act of 2019 introduced by Senator Ron Wyden (D-OR) on May 13, 2019. The bill provided that matching contribution could be made to an employee’s 401(k) account based on that employee’s student loan repayments – making the PLR’s provisions available to all. Unfortunately, Wyden’s bill didn’t make it through Congress.

But the Abbott PLR got the snowball rolling.

Using 401(k)s To Pay Off Student Loans

Congress has had employee retirement savings on its radar since before the SECURE Act (Secure 1.0) passed in December 2019. It has recognized the challenge that employees with heavy student loan debt face when trying to repay their student loans and save for retirement. Many employees make the hard decision to wait to save for retirement until their loans are paid off. That means potentially years of lost savings – savings it’s hard, if not impossible, to make up.

What’s been needed is legislation that allows employers to make matching contributions to employees who are making repayments on their student loan debt but not 401(k) deferrals, and without running afoul of compliance issues such as the contingent benefit rule.

Secure 2.0 is this legislation:

- It expands the definition of employer matching contribution to include those made to employees making payments towards qualified student loans. Plans eligible for this provision include 401(k) plans, 403(b) plans, or SIMPLE IRAs. Provisions also include governmental 457(b) plans.

- 401(k) matching contributions to help pay off student loans are subject to the same vesting schedule as are other matching contributions.

- Employers can rely on an employee’s certification to ensure loan payments are being made.

- It provides relief for actual deferral percentage (ADP) tests

-

- Student loan “matching” contributions aren’t considered matching contributions because they’re not based employee elective deferrals or after-tax voluntary contributions.

- The “matching” contributions are considered employer non-elective contributions.

- 401(k) plans are permitted to perform the ADP test separately for those participants receiving a matching contribution for student loan repayments. This allays concerns that employers’ matching contributions to these employees could skew the results of the test and make the test more difficult to pass.

-

The authors of the bill explained their thinking this way: “The idea is that employees who are overwhelmed with student debt may not realistically be able to save for retirement, and thus are missing out on available matching contributions. This legislation would allow them to receive those matching contributions by reason of repaying their loan.”

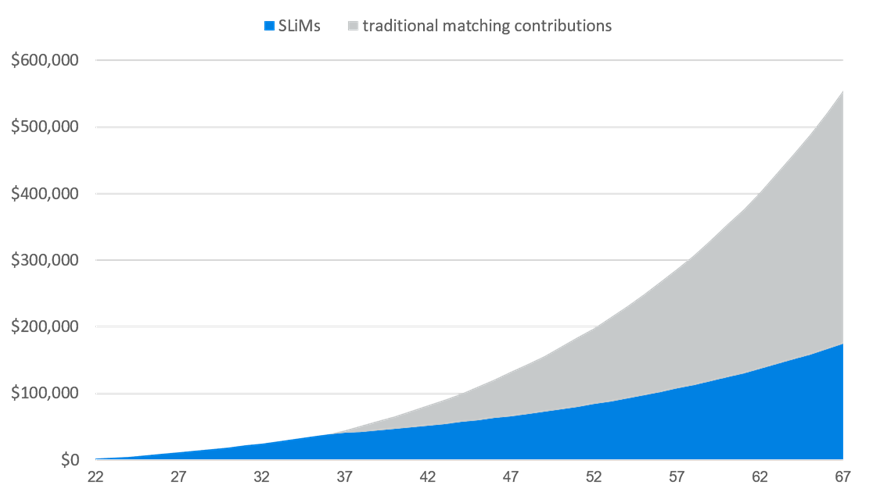

Using a 401(k) match to help employees pay off students’ loans doesn’t reduce the amount of the student’s loan, but it does help reduce the problems these employees have in saving for retirement (see Chart 2 which illustrates an example by Milliman showing the effect of how Secure 2.0 will help pay off student loan debt: savings at retirement from employer matching contributions while the loan was being paid off-in light blue-equates to almost one-third of total savings [Note: SLiMs is Milliman’s term for student loan matches.]).

Chart 2 – Growth of SLiMs (© Milliman) Made Before Employer Match

Assuming Secure 2.0 is passed by the end of this year, this provision will be effective for plan years beginning after December 31, 2022.

Conclusion

Many employers are having great difficulty in finding and retaining employees. This provision in Secure 2.0 that allows employers to offer a 401(k) match based on employees’ student loan repayments is sure to prove popular with current and prospective employees.

So, if you or any of your clients or prospects are wondering if this provision (if passed) can help them with their employment challenges, they’re in luck.

We in the Pension Division at RMC Group specialize in working with advisors who serve the small plan market. We can help you market, set up, and administer your clients’ profit-sharing or other qualified plan, and when the time times, can help you set up student loan repayment programs.

Call 239-298-8210 or visit our website at rmcgp.com to discover how we can partner with you to help small businesses successfully set up and administer a profit-sharing plan.

-Jun-01-2026-09-11-11-7643-PM.png)

-May-28-2026-04-06-00-2941-PM.png)