About half of private-sector employees in the United States – over 55 million Americans, many working for small businesses (those with fewer than 100 employees) – don’t have access to any type of workplace retirement plan because their employer doesn’t offer one.

This has created a huge savings gap in the United States despite the wide-spread use of the popular 401(k) plan.

Frustrated, a grass-roots movement in the retirement industry sprang up 10 years ago to see what could be done, and the states decided to step up and get into the retirement business – they would offer their own retirement plans.

People prefer choice, they knew. But with the gap in retirement savings so big, made worse by the pandemic and uncertainty about future Social Security benefits, the states thought they would need to take the drastic step of making their plans, and participation in them, mandatory.

State-mandated retirement plans are created by laws passed by a state’s legislature. As a result of the law, small businesses are to provide a retirement plan to their employees – either the state-sponsored plan or a private profit-sharing or other qualified plan – although two states have chosen to make their plans voluntary.

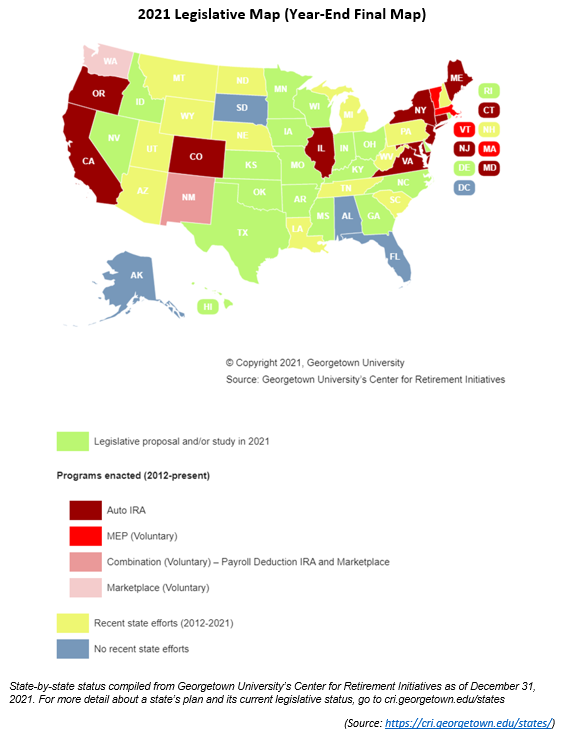

Looking at the map below, it’s easy to see that what started out as a mere trickle in 2017 has grown to a torrent as 46 states have or are considering having state-sponsored plans.

As of December 31, 2021, 14 states and two cities (though NY City’s program is expected to be merged with the NY state program and Seattle’s is on hold indefinitely pending state legislative action) have passed laws requiring private-sector employees to participate in their state retirement program unless they offer a retirement plan for their employees; more states have proposed such legislation.

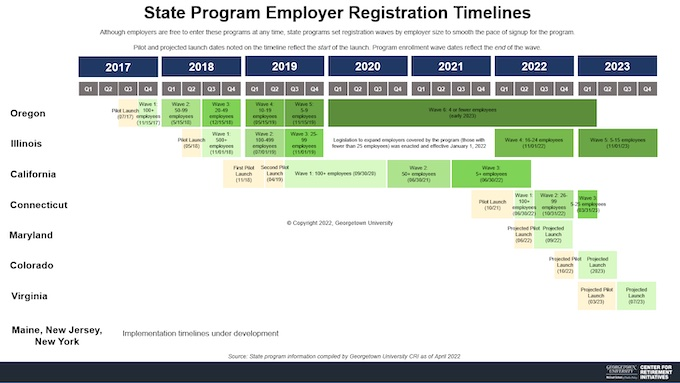

As of April 1, 2022, six of the 14 states are open to companies enrolling their employees in their plans – Oregon, Illinois, California, and Connecticut (mandatory plans) and Massachusetts and Washington (voluntary plans). The remaining states are being phased in in waves (Table 1).

Source: https://cri.georgetown.edu/states/

Although every state’s plan is different, there are some commonalities:

These plans are designed for low to moderate-income wage earners who work for small businesses, not for employees of larger companies who are more likely to have a retirement plan. And since most of the plans are Roth IRAs, high-income earners aren’t allowed to participate due to federal wage limitations for IRAs ($135,000 in 2022).

It’s important to remember that these plans are only mandatory to the extent the employer doesn’t have a profit-sharing or other type of qualified plan, which exempts an employer from participating in the state plan. That’s good, since the state plan may not be best for the best fit for the employers or employees.

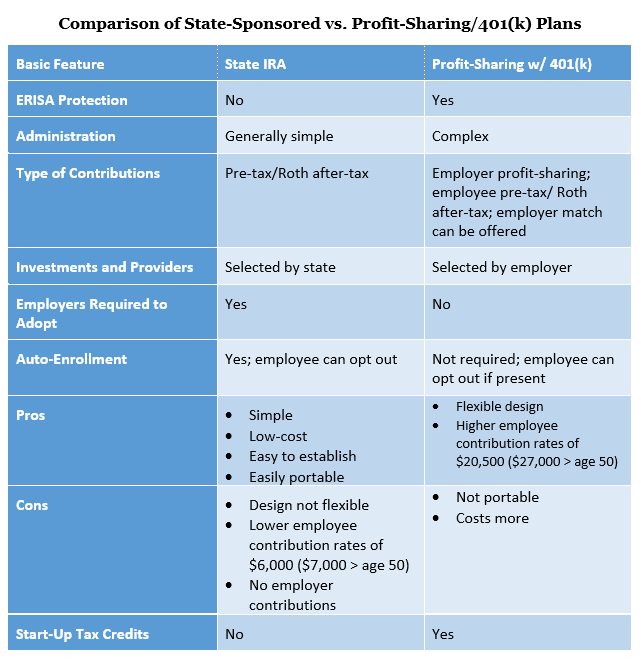

So don’t let the state mandates keep you from talking to small business owners in those states. You have an opportunity to show small businesses they have an alternative way to save for retirement – not with the state-run cookie-cutter plan – but with a profit-sharing plan designed specifically for them (see Table 4).

A profit-sharing plan has a lot of benefits not available under a state-run plan that you can discuss with business owners.

A feature to highlight is that the employer can save for his own retirement with a profit-sharing plan, something he can’t do under a state-sponsored plan. Employees are better off as well, with employer profit-sharing contributions that wouldn’t be possible under a state plan, plus employee contributions with higher limits if there’s a 401(k) feature.

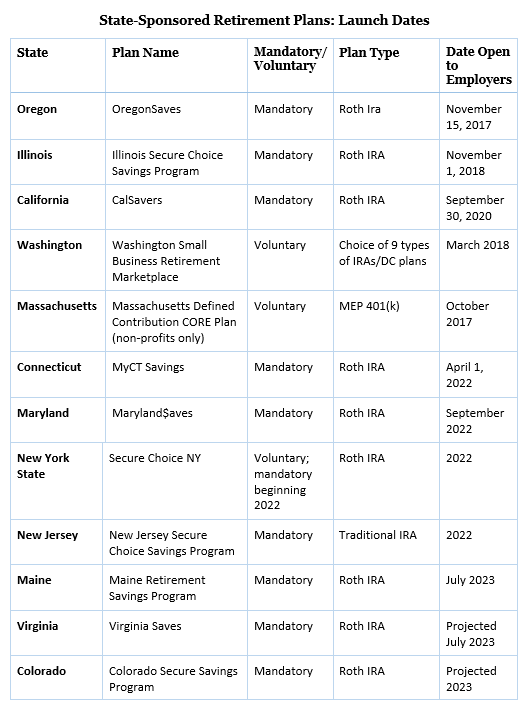

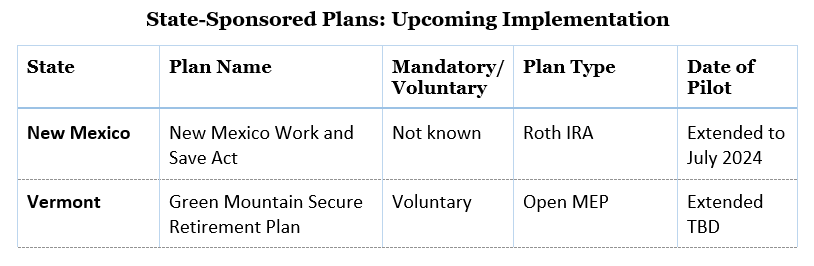

Tables 1, 2, and 3 show the states who have or are going to have state-sponsored retirement programs, and where they are in their implementation, generally phased in in waves.

Business owners in those states need to know they have choices, better alternatives. Even if they’re already enrolled in their state’s plan, they can opt out of it by adopting a profit-sharing plan from you.

By helping small businesses have a better savings plan, you’re also helping yourself. You’ll grow your business with new plans and assets that may start out as small amounts, but that give you the potential to make money down the road as they grow through on-going contributions.

We in our Pension Division at RMC Group specialize in working with advisors who serve the small plan market, the market targeted by state-run retirement programs. We can help you market, set up, and administer your clients’ profit-sharing or other qualified plan. As this article has shown, there are lots of opportunities in the states with mandated retirement plans for you to shine by showing the many benefits of alternate options such as profit-sharing plans. State-run plans don’t fit everybody.

Call 239-298-8210 or visit our website at rmcgp.com to discover how we can partner with you to help small businesses successfully set up and administer a profit-sharing plan.

So, gear up! It’s all hands on deck to give small business owners the retirement plan choices they need to have!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}