It’s April and tax season is in full swing. Why not establish a profit-sharing plan or other qualified retirement plan?

But it’s too late for a 2021 plan, isn’t it, business owners may wonder?

No, it’s not. The refrain “My Gallant Crew” from Gilbert and Sullivan’s popular H.M.S. Pinafore seems to be appropriate as the crew kept asking, “What, never?” until the captain had to say, “Hardly ever!” Businesses who were thinking of starting a retirement plan at the end of 2021, but didn’t, can rejoice on learning that it’s hardly ever too late to establish a plan. They can still have one for 2021.

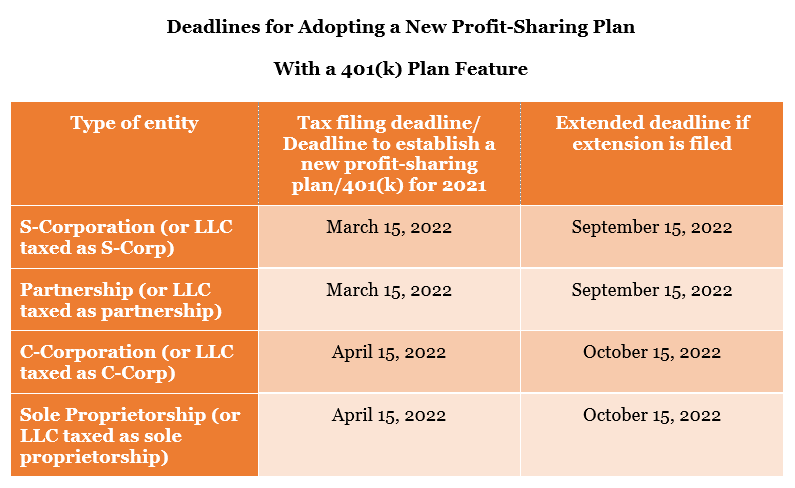

Previously, before 2020, business owners would have had to have their plan set up by the last day of the business’s tax year. For a calendar year plan that meant the documents must have been signed by December 31st of that tax year even though the company was able to take a deduction for their contributions if made through their tax filing deadline (i.e., October 15 on extension).

But everything changed with the passage of the Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE Act). For years after 2020, thanks to SECURE, businesses now have more time to set up a profit-sharing plan for a particular tax year.

The deadline now is a business’s tax filing deadline, plus extensions. This means the deadline will depend on what kind of business it is (e.g., sole proprietorship, partnership, corporation, etc.).

The same deadlines apply to owner-only businesses that may want to set up a solo plan.

A delayed plan adoption helps the employer more than it does employees. That’s because employees can’t make retroactive deferrals, but the company could make retroactive contributions for the prior year to everyone in the form of profit-sharing contributions.

Be careful, though. Pay careful attention to the deadline for filing a new plan’s first Form 5500. A plan’s Form 5500 must generally still be filed by July 31st. However, if a company’s business tax return is extended and the plan year is the same as the tax year, the company qualifies for an automatic Form 5500 extension through October 15th. It doesn’t need to file a Form 5558 formal extension request.

Regardless of the timing of the plan’s adoption, a 2021 Form 5500 will need to be filed by the applicable deadlines if established by the business’s 2021 tax filing deadlines plus extension.

Profit-sharing plans are popular, especially when paired with a 401(k) plan. They’re an excellent way for both employers and employees to save money for a more financially secure retirement and save on taxes at the same time. These plans also help attract and keep the employees the owner needs to run the business.

Setting up a profit-sharing plan takes time, though, so employers shouldn’t wait until the last minute. Qualified retirement plans are also highly regulated by the IRS, DOL, and ERISA so it’s important that they’re set up correctly and run according to Uncle Sam’s rules and regulations.

The first step in setting up a profit-sharing plan is to find a good advisor to work with. An advisor can help in identifying and retaining other provider partners to help with plan administration, payroll integration, and investments.

Starting a plan first requires a decision as to the core type of profit-sharing plan that best meets the company’s goals and objectives. Then the conversation shifts to how to design it that helps both employer and employees: employer contributions, employee deferrals, vesting, loans, hardship distributions, and types and number of investment options.

These fall into three main categories:

1. Profit-Sharing. A profit-sharing plan is a plan that gives employees a share of the company’s profits.

2. Traditional 401(k) Provision. A profit-sharing plan with 401(k) plan features can be the best of both worlds, with employee pre-tax deferrals in addition to the company’s profit-sharing contribution.

3. Qualified Automatic Contribution Agreement (QACA) Provision. A profit-sharing plan with a 401(k) auto-enrollment safe harbor provision, in which the employer must make a match or nonelective contribution, and which exempts the plan from year-end compliance testing requirements.

The 401(k) provisions have additional requirements but are attractive to employees in that they give them an opportunity to save on a pre-tax basis. Adding automatic enrollment and escalation encourages employees to save for retirement by requiring them to opt-out of contributing, which most don’t do.

Plan design decisions are then incorporated into a written plan document, often an adoption agreement with a pre-approved document. The plan document must be reviewed and adopted, and signed, by the business’s tax return deadline when a retroactive plan is adopted, along with:

Then it’s time to bring the providers that you selected with the help of your advisor on board. There is generally a one-time charge for setting up the plan and a monthly or quarterly administration charge.

Of particular importance is the investment manager who helps plan the mix of investments, investments with fund expenses as low as practicable.

Next is rolling the plan out to employees with a kick-off meeting to help them understand the plan and how participating in it will help them have a more financially secure retirement. The meeting will need to include deferral information and investment options. Plus, knowing the company has already committed to contributing will encourage employees to enroll in the plan.

The final step is to prepare and file the plan’s Form 5500 and schedules by the IRS’ deadline.

Over 50 million Americans don’t have access to a retirement plan; most of these work for a small business that doesn’t sponsor a profit-sharing/401(k) plan. For example, there are more than 30 million small businesses in the U.S., but only a total of 600,000 401(k) plans. That’s a huge gap.

So, Uncle Sam has stepped up to the plate and now offers startup cost tax credits to eligible small businesses who want to start a plan.

Tax credits for eligible small-employee profit-sharing and other qualified plans are designed to alleviate some of the startup costs as an incentive for small business owners to offer a retirement plan for their employees.

Two credits are available:

1. Startup costs. A startup tax credit of 50% of eligible startup costs up to $5,000 for each of the plan’s first three years.

2. Auto-enrollment credit. An additional tax credit of $500 per year for a three-year period for offering auto-enrollment in their plan.

That equates to up to $5,500 a year, or $16,500 over three-years for an employer who takes advantage of both tax credits.

It’s enticing.

Both employers and employees receive substantial benefits from having a qualified profit-sharing or other type of qualified plan to participate in.

Employees receive tax-deferred profit-sharing contributions from their employer, and if a 401(k) feature is part of the plan, can make pre-tax deferrals to the plan.

Employers receive tax deductions for start-up and administrative costs not covered by the start-up tax credits and are able to save for their retirement as well as providing a savings vehicle for their employees. In addition, sponsoring a profit-sharing/401(k) plan creates an exemption for that company from having to participate in their state-run IRA program (if one exists).

So, if any of your clints or prospects are bemoaning that they had really wanted a retirement plan for 2021, but just didn’t get around to it, they’re in luck. For, as the captain’s crew sang, it’s “hardly ever” too late to retroactively set up a profit-sharing plan.

We at RMC Group in our Pension Division specialize in working with advisors who serve the small plan market. We can help you market, set up, and administer your clients’ profit-sharing or other qualified plan. As this article has shown, it’s not too late for businesses to start a plan for 2021.

Call 239-298-8210 or visit our website at rmcgp.com to discover how we can partner with you to help small businesses successfully set up and administer a profit-sharing plan.

Note: If a company is even considering adopting a 2021 profit-sharing plan retroactively, they’re wise to file a tax extension and then contact an advisor to start the process as soon as possible.

{kind=link}